Introducing nCore — The Solution to Modern-day Banking Problems

In General•News posted on March 17, 2021 | by ![]() ProximaX Editorial Team

ProximaX Editorial Team

As we head further into the future, the world is only becoming more globalized in conducting business and transactions. Less than a decade ago, the world was not as effectively connected as it is today. Thanks to the internet, smartphones, and services that help people conduct business and trade with each other no matter where on the globe they are.

At the center of this expanding global economy lies our existing financial system. So far, it has efficaciously catered to this globalization by taking banking services online and changing banking infrastructure to aid smoother transactions. But the truth is, it is only a digitalized version of the paper-based banking process. If we contrast it against the growing technologies, the financial industry has shown little development.

Banking Problems at a Glance

The legacy financial system as we know it today lacks on multiple fronts. Starting from fundamental issues such as cost-intensive transaction settlement to critical ones such as security vulnerabilities, our banking infrastructure is in dire need of improvement.

International banking and transaction services remain complex, time-consuming, and expensive as geographical boundaries restrict the existing financial infrastructure. The services banks offer are restricted to their country, forcing them to rely on third parties to process international transactions. This not only affects end-users but also levies hefty costs on banks.

Besides, banks operate on centralized servers that are vulnerable to cyberthreats. This requires banks to spend millions of dollars annually to secure their servers to prevent the theft of funds and data.

nCore — The Blockchain Solution

Blockchains perform only one function — record information about different types of transactions. But they do the job so flawlessly that they have entirely shifted the momentum of major industries by changing how they record and store data.

When blockchain was introduced, its only use was to facilitate peer-to-peer transactions. Over the years, however, new types of blockchain infrastructures have been developed that perform the same task differently and extended to a wide range of use cases. Even then, the vast impact it can have on our existing financial system is unparalleled by other use cases.

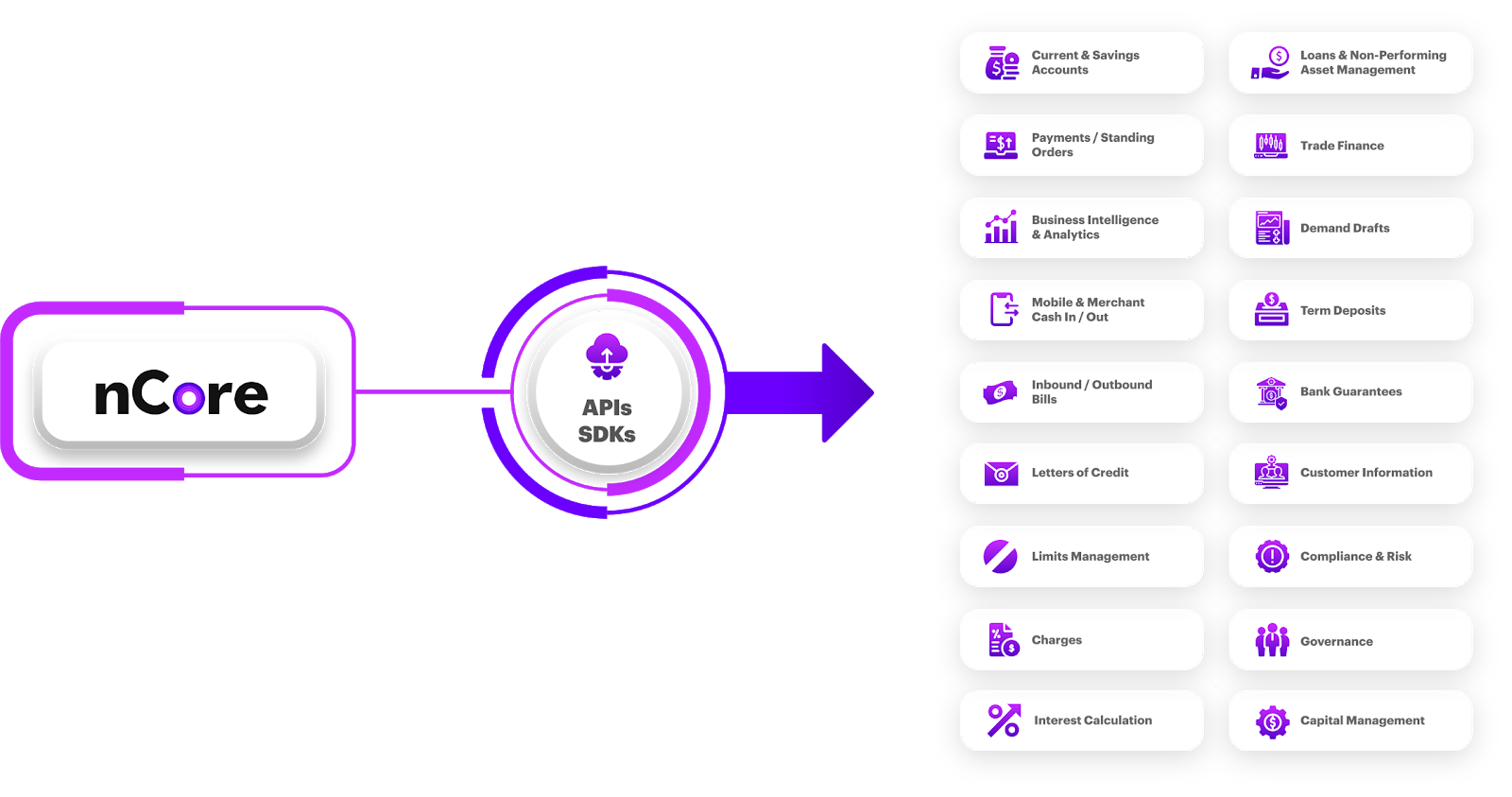

This is why we developed nCore, a neobanking core system powered by ProximaX’s blockchain technology. nCore is specifically designed to help make digital banking services more comprehensive and efficient.

Leveraging the distributed infrastructure of blockchain combined with its cryptographic security allows nCore to offer heightened resilience against attack vectors. Digital banking service providers can utilize nCore as their base infrastructure and integrate third-party services using easy-to-use APIs and SDKs. Service providers can then offer the same services as they do now but only in a better manner by taking the benefit of blockchain’s security, transparency, and high scalability.

Figure 1. An open system

Besides, ProximaX’s nCore takes a slightly different approach to blockchain than its competitors to ensure the best enterprise-grade performance. Let’s take a look at what sets nCore apart from other blockchain solutions for digitalized banking.

Prime Features of nCore

nCore is a blockchain solution that stays a class apart from its competition by delivering solutions rare in the whole industry. Here’s a quick overview of the primary nCore features that banking service providers will benefit from:

- Account restrictions: Traditionally, blockchains are open networks that allow anyone in the world to pay and receive payments from anyone else. However, as an enterprise-grade solution, it is critical for nCore to depart from the traditional definition and create room for certain restrictions. For one, the account restriction feature of nCore allows users to create a list of permitted addresses that can send payments to their accounts. Payments from all other addresses are rejected.

- Lost account recovery: Almost all blockchain solutions do not have the ability to recover from a lost account key – the most important criterion for mainstream financial industry requirements. If a customer loses her key to an account, ProximaX stands out among the rare few blockchain solutions that can recover the account. The lack of this feature has been one of the most prohibitive reasons that make a blockchain solution unacceptable for neobanking until now.

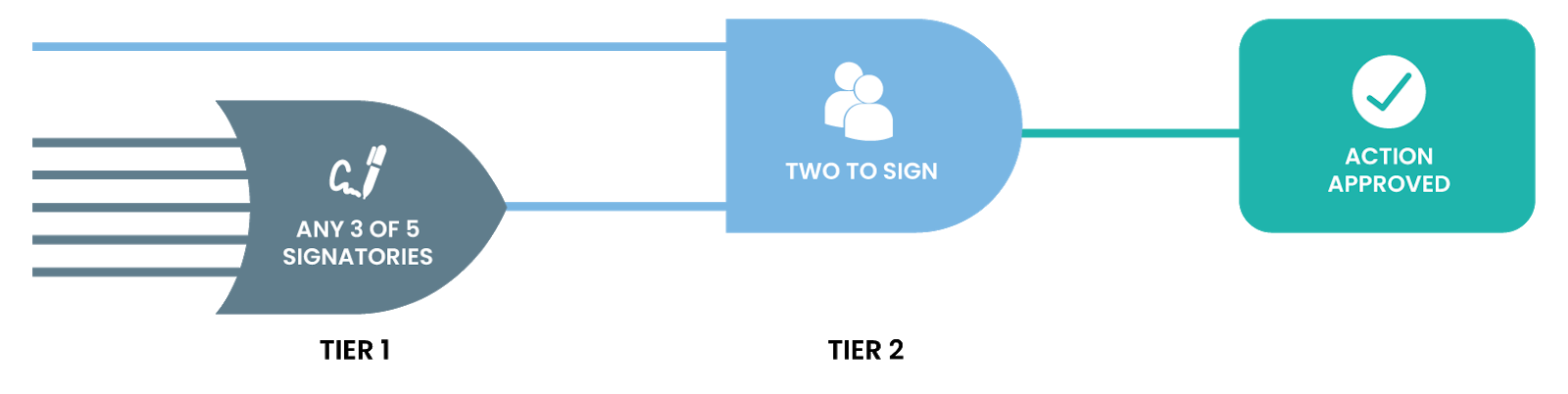

- Multi-level multi-signature accounts: Very often, transactions at the enterprise level require the approval of multiple parties at several levels. nCore’s multi-level multi-signature accounts allow multiple signatories to agree on a said transaction before executing it. Enterprises can specify the minimum number of signatures required to execute a transaction or remove a signatory.

In addition, the multi-level feature helps to escalate the transaction from one level to the other for final execution. Every time a required number of signatories approve a transaction, it will be forwarded to the next level and so on. This creates a multi-layer transaction approval process that is not possible on all blockchain infrastructures.

Figure 2. Multi-level multi-signing of a transaction

- Aggregate transactions: Using aggregate transactions, nCore allows combining multiple banking transactions into one transaction. This can be used for trust-less swaps, escrows, and other advanced transaction logic. However, for this to happen, all authorized signatories must sign the transactions to automatically and irrevocably execute the exchange.

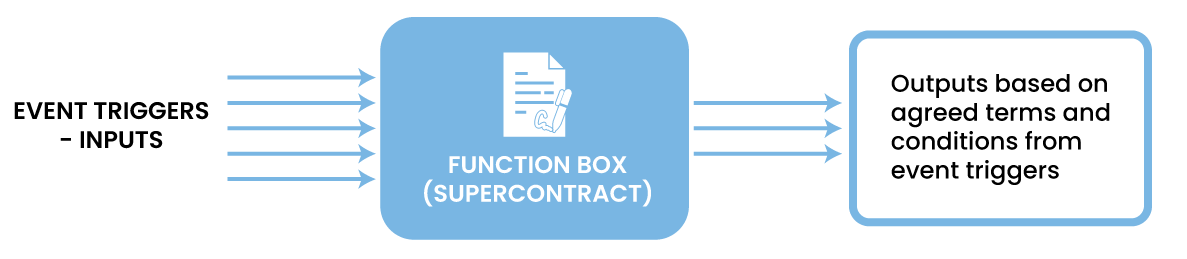

- Supercontracts: Smart contracts have become an important part of the entire blockchain ecosystem. They are self-executing computer functions that can allow multiple parties to collaborate and execute various transactions without the need for an intermediary. Developers can program these contracts to trigger certain actions depending upon the occurrence of some mutually agreed event(s).

For example, a smart contract can be used to pay EMIs every month (action) on a specific date (event). Or, the payment to a freelancer can be released (action) when the task at hand is completed (event). We can apply the same logic to many transaction scenarios.

Supercontracts on nCore are an improved version of smart contracts that are located off-chain in ProximaX’s distributed and decentralized storage layer. While smart contracts are difficult to modify, Supercontracts allow authorized parties to easily stop, amend, and restart them if they reach a consensus.

Figure 3. A typical representation of a Supercontract

- Metadata: Metadata is important in conveying a message with certain transactions and banks can do so using nCore. For example, if a bank wants to prohibit transactions to a blacklisted account or prioritize transactions to some special accounts, they can apply metadata along with the funds or the accounts directly to add more information.

- Cross-chain swaps: Cross-chain swap or atomic swap is a way to transact between two different ledgers having an independent network. Given the right architecture and design, nCore offers an atomic swap-friendly infrastructure so users can easily and instantly transact funds irrespective of what bank blockchain network they have their accounts in.

Leveraging ProximaX’s Fintech Solutions

nCore in itself offers a wide range of features combined with the inherent advantages of blockchains. But that’s not it. As nCore uses a modularized framework, bank operators using nCore can further integrate other fintech solutions by ProximaX.

While ProximaX powers a variety of high-potential solutions, two of its most prominent ones are SiriusKYC and mWallet. Let’s take a quick look at them.

- SiriusKYC by ProximaX: SiriusKYC is a “Know Your Counterparty” solution developed on top of the ProximaX Sirius development platform. It is a W3C-compliant state-of-the-art digital identity solution that uses ProximaX’s self-sovereign identity (“SSI”) technology.

The KYC solution enables bank operators and service providers to link every bank account to a digital identity on the ledger. This is an essential element for banks to stay updated on all transactions linked to every digital identity. By tracking the transactions related to a digital identity, they can easily flag those transactions as well as the identity owner.

If used alongside digital money, digital identity and the KYC process can significantly reduce tax evasion and illicit transactions while providing vital data for improved bank monetary and fiscal policies.

- mWallet by ProximaX: mWallet is ProximaX’s white-label mobile wallet powered by blockchain technology. Apart from allowing normal functionalities like bill payment and remittances, mWallet is relatively inexpensive, scalable, and reliable than other traditional mobile wallets. mWallet is fully customizable and can be converted into a mobile banking service or a full-fledged neobanking solution as it uses the same nCore base infrastructure.

Besides, mWallet allows third-party integration from payment gateways to accounting systems. It also allows users to recover funds in case the wallet is lost or stolen. All in all, mWallet can be a highly valuable solution for financial service providers.

Closing Thoughts

Blockchain is undoubtedly poised to disrupt the existing financial system and make it faster, more efficient, secure, and user-centric. And with many major banks experimenting with and implementing blockchain, it now seems inevitable for more and more financial institutions to follow suit. As that happens, and given that most blockchains cannot match some of the requirements of the financial industry, ProximaX’s nCore is the best in class for banks to tread into the blockchain space and integrate this groundbreaking technology into their infrastructure.

Learn more about nCore here.

Subscribe to ProximaX blog updates!

Keep up with our latest technology news and announcements.